18 stats to understand the future of CX optimization and banking

Businesses that discover and apply customer insights are more likely to grow revenue, acquire more customers, and stand out from their competitors. That's because more people want seamless, quality banking services online.

Yet, consumers are not satisfied with their experiences with digital products available today. It's clear that banks are falling behind other industries in optimizing their customer experience—but why?

These statistics, collected from the latest research about digital banking and CX, should give banks and financial services providers food for thought about where they can improve. They also provide insights into where competitors fall short so digital-first organizations can pull ahead.

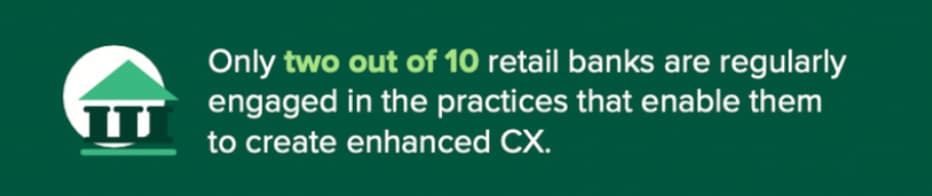

1. Only 2 out of 10 retail banks are regularly engaged in activities that enhance customer experience.

Coming from a recent Forrester report on CX in banking, this stat means that out of the 107 managers and directors responsible for marketing and customer experience at North American retail banks, only 20% are actively optimizing customer experiences. It’s not that retail banks don’t understand the importance of a strong data management strategy—they just don’t know how to put it into action.

2. Retail banks that regularly practice customer experience optimization grow 3.2x faster than competitors that don’t.

A clearly defined CX strategy coupled with the right execution leads to faster growth. Because we live in an era of hyper-personalization and on-demand services, businesses that do not refine their CX strategy quickly fall behind the others. On the flip side, businesses that leverage the right tools and technologies in optimization grow exponentially.

3. Over 70% of retail banks believe that digital customer engagement is important to the success of their businesses today and tomorrow.

The advancement of technology, the adoption of mobile/online banking, and the COVID-19 pandemic have made digital customer engagement a top priority for banking leaders. New technologies present banks with opportunities to become first-movers so that they can differentiate their products. The adoption of online/mobile banking coupled with the pandemic means that businesses need an on-demand, multi-device, omnichannel, data strategy to better serve their customers.

4. Only 38% of banks see their data strategy as very mature.

Data is only as good as the insights it produces, the actions it influences, and the results it fosters. An immature data strategy, which the stat indicates is a major problem, means a poor understanding of customer insights and how to leverage them to create better customer experiences at scale.

5. 70% of CX data is collected from digital interactions. Of that 70%, only 59% is acted on to improve customers’ digital experience.

This means that most banks are over-collecting and underoptimizing. Data collection is prioritized data analysis isn’t. This could point to a problem of a lack of resources or technological limitations around data analysis. It may also point to an issue of scarcity with quality data analytics professionals. Lastly, it could point to a fear of CX leaders around using the customer data they collected.

6. The top 3 digital experience optimization techniques retail banks employ include rule-based targeting (36%), profile-based targeting and personalization (32%), and A/B testing (31%).

Businesses should use a wide array of customer insights techniques to provide better digital experiences. These digital optimization techniques provide businesses with a more nuanced view of every customer visit and help them optimize experiences across channels. The consistent application of digital experience optimization techniques separates top performers from the rest.

7. Research shows that 86% of retail bank customers are willing to share their data to personalize their banking experience.

Data privacy is a genuine concern for many retail bank customers. With laws like GDPR and CCPA picking up and the rampant data breaches plaguing every industry, data privacy concerns will only grow from here on out. Banks should be transparent in disclosing how customer data is being used to avoid data privacy violations and the loss of their customers’ trust.

8. Banks trail consumers’ favorite brands by at least 12% in making emotional connections.

According to the Deloitte report, "as banks embrace varied strategies to differentiate themselves, they need to pay close attention to how they make their customers feel so they can build sticky relationships." Whether that means making it easier to purchase products, curating personalized recommendations, or making easier sign-up processes, financial services institutions need to increase their CX experimentation to stop falling behind. .

9. Consumers still prefer traditional channels (eg. speaking to a rep in person) when handling complex issues.

Credit card inquiries, home equity loans, mortgage refinancing are examples of issues that require greater advisory services. This could point to distrust customers of the retail banks have of the current technologies to handle the sensitive financial information required for loans, mortgages, and wealth management services.

10. Contacting customers through their preferred channel can boost installment payment upticks by more than 10 percent.

The devastating financial impact of the pandemic means that collections operating methods need to be rethought in 2021 and beyond. Banks need to find a way to balance empowering their customers to a brighter financial future and managing credit losses.

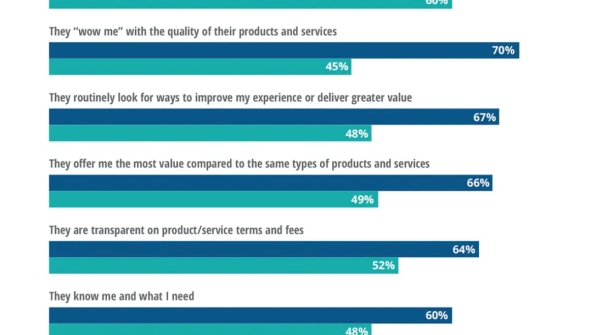

11. 76% of customers reported that their expectations are being met. Only 9% of respondents say their expectations are being exceeded.

This suggests that there is room for improvement for banks to “wow” their customers. Banks have to think outside of the box to put together compelling CX strategies across communication channels, products, and services.

12. 79% of customers who managed their portfolio identified simplicity as key importance.

This suggests that creating easy-to-use UX is still a struggle for many banks. Overly complex services, products, and communication are sure to turn off digital-first customers that value simplicity. The challenge for banks is to simplify their offerings and communication without compromising quality and clarity.

13. 55% of CIOs at global banks cite improving client experiences as the top priority.

Improving digital experiences requires a laser focus on the customers. Centering customer emotion in the product development process, testing ideas quickly with customers, and creating feedback loops/being accessible are some techniques banks can use to improve their CX.

14. 8 out of 10 customers take some form of action after a bad experience.

35% tell friends, family, or colleagues, 30% complain in person, and 16% start to use the company less. U.S. and French customers are more likely to reduce their patronage of the bank (21%) compared to their UK and German counterparts (11%)

Negative experiences can be amplified through word of mouth and social media. This negative spread damages a bank’s reputation and can lead to higher churn. Modern banking needs to be on-demand and hyper-personalized to start “wowing” customers.

15. Just over half of consumers feel financially comfortable or secure versus 43 percent who feel overwhelmed or vulnerable.

Remote work allowed many customers to save money that would otherwise be spent on commutes, expensive city rent, takeout, office clothes, and more. Many accumulated wealth during the pandemic through more savings and lifestyle changes, thus feeling more comfortable financially. Banks should increase their product offering personalization to connect with different consumers.

16. Out of 1299 CX leaders surveyed, over half (52%) of respondents are investing in at least six out of the top 8 customer-centric capabilities.

Greater connectivity amongst all parts of the banking system is needed to surpass customer expectations. For example, connecting insights-driven strategies to innovative services to experience-centricity by design creates a more seamless banking experience for every customer.

17. The top three challenges to improving the customer experience in the digital age are outdated technology (49%), siloed systems (48%), and the lack of a consolidated customer view (42%).

Banks should evaluate all touchpoints in the customer journey and collect useful data using engaging, but non-intrusive techniques such as personalized pop-ups. A clear, nuanced understanding of the customer experience can help banks take actions so that they exceed customer expectations.

18. A change in CX rating has huge consequences in the banking industry — for a multichannel bank, losing just one point translates to $124 million left on the table.

CX has a strong correlation with a financial institution’s branding and revenue. It’s crucial for banks to prioritize digital experience optimization by running regular tests and leading their data strategy with the customer’s needs at the center.